If you have a Blue Cross Blue Shield of Michigan plan and you — or anyone in your family — receives care through University of Michigan Health, there is something important happening right now that you need to understand before July 1. A contract dispute between Blue Cross and Michigan Medicine has set a deadline that could change what you pay for care at some of the most relied-upon facilities in our region. Here’s a plain-language explanation of what’s happening, what it means for your specific plan, and what steps you can take to protect yourself.

What Is the Blue Cross / Michigan Medicine Dispute?

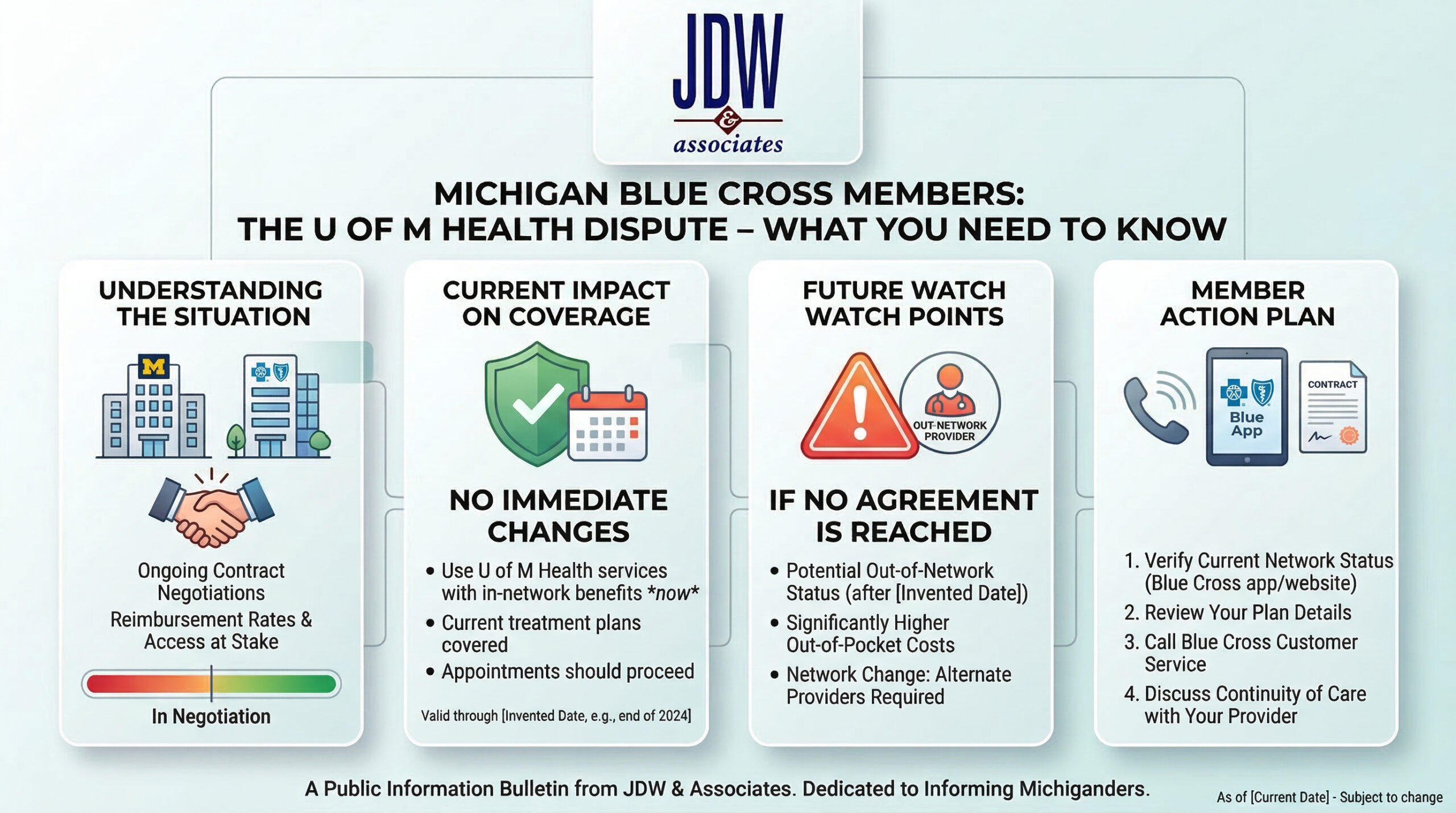

Earlier this month, Michigan Medicine — the University of Michigan’s hospital and health system — formally notified Blue Cross Blue Shield of Michigan that it intends to exit the Blue Cross network as of July 1, 2026, unless both parties reach a new contract agreement before that date. The dispute centers on reimbursement rates: the two organizations are publicly disagreeing over the terms, with Michigan Medicine saying Blue Cross has proposed cuts to what it pays the health system, and Blue Cross saying Michigan Medicine’s demands are too high. The specifics of who’s right matter less to patients than what happens if no deal is reached.

According to reporting by the Detroit News, more than 300,000 Michigan Medicine patients could be affected. The facilities at risk of going out of network include University Hospital, C.S. Mott Children’s Hospital, Von Voigtlander Women’s Hospital, the Frankel Cardiovascular Center — and, closer to home, the Chelsea Health Center, the West Ann Arbor Health Center, the Briarwood Medical Group, and associated outpatient clinics across Southeast Michigan. For Washtenaw County residents, this is not a distant headline. It could directly affect the specialists, physicians, and care teams you rely on.

What This Means Depends on Your Plan Type

This is the part most people don’t know — and it’s the most important detail in this entire situation. What happens to your costs if a deal isn’t reached depends entirely on whether you have an HMO or a PPO plan through Blue Cross.

If you have a Blue Care Network HMO plan, your plan provides zero out-of-network benefits. If Michigan Medicine goes out of network and you seek non-emergency care there, you could be responsible for 100% of those costs out of pocket. There is no shared cost with your insurer — your insurance simply does not cover out-of-network care under an HMO structure.

If you have a Blue Cross PPO plan, you do have out-of-network benefits, but you will pay significantly more. According to Blue Cross’s own guidance, out-of-network costs are typically double what you would pay in-network. A specialist visit that costs you $60 in-network could become $120 or more. A procedure or hospital stay could mean thousands of dollars in additional cost.

There is one important exception: Blue Cross has indicated that patients with certain serious conditions — including cancer, cardiovascular disease, diabetes, autoimmune disorders, Alzheimer’s disease, pregnancy, and others — may qualify for a 90-day “Continuity of Care” period that extends in-network rates temporarily. But that’s a 90-day window, not a permanent solution, and it requires you to know about it and apply.

Can You Switch Plans if a Deal Isn’t Reached?

This is the question we hear most often in situations like this, and the answer is an important one: no, a contract breakdown between a hospital and an insurer does not qualify as a special enrollment event. Blue Cross has confirmed this directly — you cannot switch to a different insurer mid-year simply because Michigan Medicine may leave the network. Your next opportunity to change your health plan would be the 2027 open enrollment period, which begins November 1, 2026.

This makes the next few months more important than they might seem. Understanding your current plan, knowing what your options are, and making sure your coverage actually fits your care needs — before July 1 — is the smartest move you can make right now.

The Bigger Picture: You May Already Be Paying More Than You Should

The Blue Cross / Michigan Medicine situation isn’t happening in isolation. If you’re a Michigan resident who buys your own individual or family health insurance, 2026 has already brought real financial pressure. Michigan’s individual marketplace premiums rose an average of 20.2% this year, and Blue Cross Blue Shield plans specifically increased by 23-24%. On top of that, the enhanced federal premium tax credits that reduced costs for millions of Michigan residents expired on December 31, 2025.

What many people don’t know is that this year, insurers were not required to include the new 2026 premium amount in the renewal notices they sent to existing customers. If you auto-renewed your plan without logging into HealthCare.gov to check your new rate, you may have seen a significantly higher bill in January or February without any warning. And if your income or household situation changed in 2025, you may be eligible for a different level of subsidy that you haven’t been receiving.

For self-employed professionals, small business owners, and independent contractors in the Chelsea and Washtenaw County area, these compounding changes — higher premiums, reduced subsidies, and now a potential network disruption — make a thorough coverage review more valuable than ever.

What You Can Do Right Now

You don’t need to wait and see how the Blue Cross / Michigan Medicine negotiations resolve. There are practical steps you can take today to understand your exposure and protect your coverage.

First, find out whether you have an HMO or PPO plan. This single detail determines your entire risk profile if a deal isn’t reached. Your insurance card will show this, as will your plan documents or your member account on BCBSM.com.

Second, identify which of your providers and facilities are associated with Michigan Medicine’s academic medical center — not just U-M Health Sparrow or U-M Health West, which are not part of this dispute. If you see specialists, use outpatient clinics, or receive ongoing care within the affected network, you’ll want to understand your options before July 1.

Third, consider having an independent coverage review with an advisor who works for you — not for the insurance company. At JDW & Associates, we work with multiple carriers and can help you understand what your current plan actually covers, whether there are alternatives worth considering, and what protections exist for your specific situation.

We’re Watching This So You Don’t Have To

Situations like this are exactly why having an independent insurance advisor matters. We don’t just help you find coverage during open enrollment — we stay with you through the changes that happen in between. As the Blue Cross and Michigan Medicine negotiations continue toward the June 30 deadline, we’ll keep monitoring developments and sharing what matters most for our clients in Chelsea and Washtenaw County.

If you have a Blue Cross plan and you’re uncertain what this dispute means for your family or your business, we’re here to help you get clarity. No pressure, no jargon — just a straightforward conversation about your coverage and your options.

Request a complimentary, obligation-free insurance review today. It takes less than an hour and could save you thousands before July 1.

This information is general and not legal or tax advice. Insurance coverage, rates, and availability vary by individual circumstances and are subject to change. Contact JDW & Associates for personalized guidance on your specific situation.