It’s late April. If you bought your own health insurance for 2026 — or if you decided to skip it — there’s something worth checking this week. The biggest health insurance mistakes of 2026 won’t happen in November. They’re happening quietly right now, in April and May, when income shifts, life changes, or the cost of premiums keeps people on the sidelines. The good news: there’s a 60-day window most Michiganders don’t know they have, and a quiet rule change most enrollees haven’t heard about. Both are worth a few minutes of your attention.

If You Skipped Coverage in January, You May Still Have Options

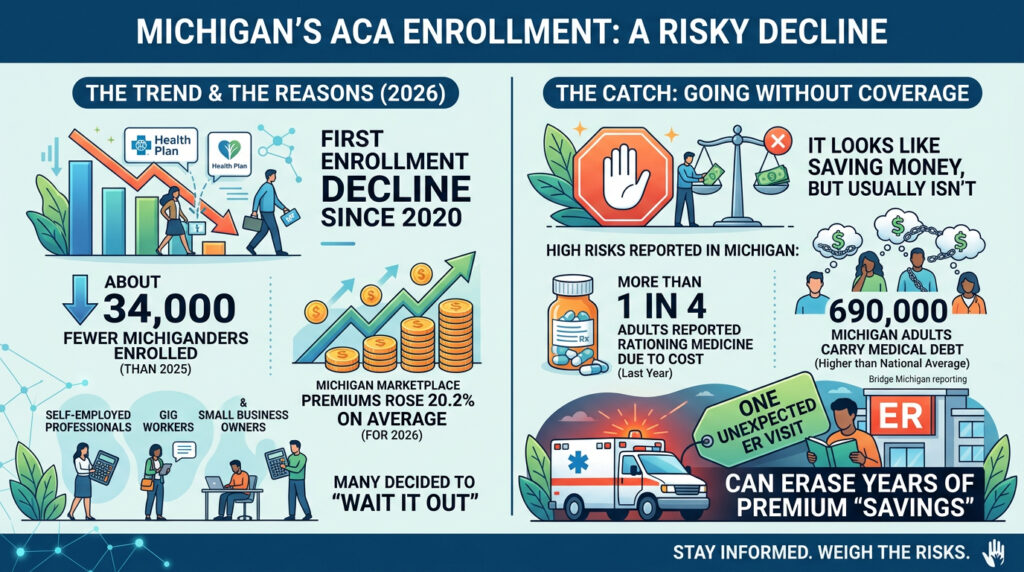

You’re not alone. About 34,000 fewer Michiganders enrolled in 2026 ACA plans than the year before — the first decline since 2020. After Michigan marketplace premiums went up 20.2% on average for 2026, plenty of self-employed professionals, gig workers, and small business owners did the math and decided to wait it out.

The catch: going without coverage looks like saving money, but it usually isn’t. More than 1 in 4 Michigan adults reported rationing medicine due to cost last year, and the same Bridge Michigan reporting found that 690,000 Michigan adults carry medical debt — a rate higher than the national average. One unexpected ER visit can erase years of premium “savings.”

If your situation has changed since January — a new job, a job loss, a marriage, a divorce, a baby, a move, or losing coverage you had through a spouse or parent — you likely qualify for a Special Enrollment Period. That gives you 60 days from the qualifying event to enroll in a Marketplace plan with full subsidy eligibility. We covered the basics in our earlier post on what to do if you missed Michigan’s open enrollment deadline, and the same options apply now.

If You Have Coverage, There’s a New Rule You Should Know About

Here’s the part most enrollees haven’t heard. Starting with the 2026 tax year, a provision in the One Big Beautiful Bill Act removed the cap on how much excess Advance Premium Tax Credit you have to pay back. In plain English: if your actual 2026 income ends up higher than what you estimated when you enrolled at HealthCare.gov, you owe back every dollar of subsidy you received above what you were entitled to. There’s no longer a ceiling on that repayment.

For W-2 employees with steady paychecks, this is usually a non-issue. For self-employed Michiganders, freelancers, small business owners, and anyone with variable or commission-based income, it’s worth a serious look. A good year that pushes your income above what you projected — or above the 400% federal poverty level threshold entirely — can turn a manageable tax bill into a much larger one.

The fix is straightforward. HealthCare.gov lets you update your income estimate at any time during the year. If your 2026 numbers are tracking differently than you projected back in November, updating now adjusts your monthly subsidy for the rest of the year and reduces the size of any reconciliation at tax time. The window doesn’t close — but the longer you wait, the less the adjustment can help.

What a Mid-Year Check-In Actually Looks Like

This is the kind of conversation health insurance is supposed to involve and usually doesn’t. A few questions can clarify a lot:

For people without 2026 coverage: Has anything changed in your life since January that might qualify you for a Special Enrollment Period? Are you eligible for Medicaid or the Healthy Michigan Plan based on your current income? Would a short-term medical plan or catastrophic coverage make sense as a bridge? Could a Health Savings Account paired with the right plan offer tax advantages you’re not currently getting?

For people with 2026 coverage: Is your income tracking with what you estimated? Do you have a major income event coming this year — a contract, a sale, a Roth conversion — that could push your numbers past where you planned? Does the plan you picked still match the providers you’re actually using? Has the BCBSM and Michigan Medicine contract dispute changed which network you should be in?

None of these questions take long to answer. All of them are easier with a local broker who knows Michigan’s market and isn’t trying to sell you a single carrier’s plan.

The Year-Round Difference

Most people only think about health insurance twice a year — at open enrollment and when something goes wrong. The middle is where the money is, both in cost savings and in avoided surprises. Income updates, plan tweaks, network checks, and Special Enrollment paths all happen between November and November — and they all reward people who pay attention before tax season hits.

If you’re not sure where you stand on your 2026 coverage, or whether a Special Enrollment Period applies to your situation, that’s exactly the kind of question we help Chelsea-area residents and small business owners work through. No pressure, no commitment — just a clearer picture of where you are and what your options look like from here.

Request a complimentary, obligation-free insurance review — or call us directly at 734-475-1664. Whether you’re enrolled, uninsured, or somewhere in between, late April is a good time to check in.

This information is general and not legal or tax advice. Insurance coverage, rates, and availability vary by individual circumstances and are subject to change. Contact JDW & Associates for personalized guidance on your specific situation.